The crypto community is lashing out against Coinbase’s reasoning for delisting Wrapped Bitcoin (WBTC) after the exchange linked the decision to the “unacceptable risk” associated with Tron founder Justin Sun.

On December 17, Coinbase filed a response to a lawsuit from BiT Global, a company affiliated with Sun. The lawsuit accused the exchange of harming the Wrapped Bitcoin (WBTC) market by removing the token from its platform in November.

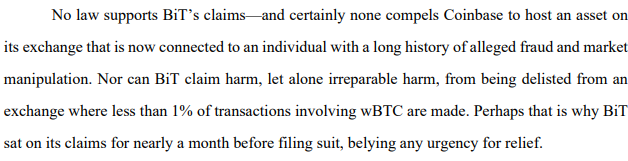

In its filing, Coinbase referenced concerns about Sun, citing allegations of financial misconduct and ongoing regulatory investigations as reasons for the delisting. According to the exchange, Sun’s involvement in the WBTC project presented significant risks that could compromise its platform’s integrity.

However, this explanation has sparked sharp criticism within the crypto community, with many questioning the adequacy of Coinbase’s legal and technical justification for the move.

Bit Global: WBTC delisting is ‘ill-advised’

In the lawsuit that BiT Global filed on December 13, it argues that the delisting was illegal and would lead to irreparable damage to WBTC’s economics. The lawsuit also criticized Coinbase for listing other tokens, including memecoins, which BiT Global claims are less serious than WBTC.

Moreover, BiT argues that COIN’s launch of its own tokenized Bitcoin product, cbBTC, breaches antitrust laws and could lead to a monopoly in the tokenized Bitcoin market, potentially stifling competition.

The exchange’s filing justified the delisting by pointing to Sun’s alleged past misdeeds, including accusations of fraud and market manipulation. It expressed skepticism about BiT Global’s credibility, highlighting the firm’s ties to Sun.

The exchange contended that its internal process led to the decision to delist WBTC, based on concerns that continued association with Sun could jeopardize its platform’s security and customer trust.

Despite this, BiT Global’s legal request to reverse the delisting claims that Coinbase’s decision was arbitrary and without merit, suggesting that the delisting would harm the token’s liquidity and market value.

Crypto community uproar ensues

Bitcoin enthusiasts and critics of the exchange, such as the prominent figure Pledditor, have lambasted the exchange’s actions, accusing it of relying on a tenuous rationale to remove WBTC.

In a post on X, Pledditor described Coinbase’s decision as “guilt by association,” arguing that the exchange’s animus toward Sun overshadowed any solid legal or technical foundation for the move.

So in a court filing today, @Coinbase gave their reason why they delisted wBTC, and it’s basically just they don’t like Justin Sun.

That’s really just it.

They don’t give any technical or legal arguments about why wBTC can’t be listed. It’s just guilt by association pic.twitter.com/bJmMnAue7x

— Pledditor (@Pledditor) December 17, 2024

The crypto exchange’s justification also faces scrutiny due to its own legal challenges. Sun, who has been the target of multiple regulatory investigations, is facing charges from the U.S. Securities and Exchange Commission (SEC) for alleged violations, including fraud.

Adding to the debate, VanEck adviser Gabor Gurbacs highlighted the irony in COIN’s stance against Sun, pointing out that the exchange itself is embroiled in significant legal battles. Gurbacs noted that Coinbase, which is under investigation by the SEC for allegedly offering unregistered securities, is hypocritical for focusing on Sun’s alleged misconduct while facing its own regulatory challenges.

It’s ironic that @coinbase is treating @justinsuntron this way. Coinbase itself is under SEC and numerous other investigations, probably many more than Justin and his businesses. Questioning someone’s reputation this way might just bring out skeletons from their own closet. https://t.co/LsJx7iOhJR

— Gabor Gurbacs (@gaborgurbacs) December 17, 2024

Meanwhile, the crypto exchange is also facing charges from the SEC, including one filed in June 2023, accusing the exchange of offering unregistered securities through various tokens listed on its platform.

Coinbase’s Chief Legal Officer, Paul Grewal, publicly called for a more constructive approach from regulators toward the cryptocurrency industry.

In addition to the SEC investigation, Coinbase also settled with the New York Department of Financial Services in January 2023 for $100 million, addressing concerns about its compliance program.

Land a High-Paying Web3 Job in 90 Days: The Ultimate Roadmap

This articles is written by : Fady Askharoun Samy Askharoun

All Rights Reserved to Amznusa www.amznusa.com

Why Amznusa?

AMZNUSA is a dynamic website that focuses on three primary categories: Technology, e-commerce and cryptocurrency news. It provides users with the latest updates and insights into online retail trends and the rapidly evolving world of digital currencies, helping visitors stay informed about both markets.